Berkshire Hathaway, under the leadership of Warren Buffett since 1965, has traditionally relied on two primary value drivers: a substantial investment portfolio known for its market-beating returns–now ~$380 billion in size–and a collection of wholly-owned businesses (subsidiaries). Historically, Berkshire's stock consistently outperformed the S&P 500; however, since around 2008, the S&P has slightly outperformed Berkshire's stock.

Our thesis is straightforward: Berkshire Hathaway should officially de-emphasize the importance of its investment portfolio by selling down positions to reduce concentration, pay the resulting capital gains tax, greatly increase portfolio diversification, and return a significant portion of the proceeds to shareholders through buybacks and dividends. (While the idea of Berkshire returning capital through buybacks and instituting a dividend isn't new, officially downplaying the investment portfolio's importance is not something we have heard discussed, and furthermore, we firmly believe it's the right action for the company.)

While Berkshire’s investment portfolio is less than half of its asset base on a mark-to-market basis, it represents an outsized driver of Berkshire’s total return. One significant contributor to Berkshire's recent returns has been Warren Buffett's strategic investment in Apple, which has yielded ~$140 billion in unrealized gains since 2018. This accounts for roughly half of the Berkshire stock performance since his Apple purchase. If not for Apple, Berkshire would have woefully underperformed the S&P. We believe this outsized success from only a single name in the portfolio is unlikely to be repeated in the future.

Warren Buffett's investment portfolio successors, Todd Combs and Ted Weschler, manage roughly $17 billion each (as of his 2021 letter) but have yet to make any significant investments. Managing a $380 billion portfolio with high concentration and large embedded gains is a daunting task, and so far it has been totally unclear how this transition will be executed. The lack of clarity surrounding this transition poses accountability challenges. If a core holding like Apple, which represents 50% of the investment portfolio, encounters difficulties, it's unclear who will have the authority to make crucial decisions.

An accounting change in 2018 brought all unrealized gains and losses in the portfolio directly into Berkshire's GAAP earnings, subjecting it to heightened scrutiny. We do not believe the same patience with portfolio fluctuations that has been extended to the greatest investor of all time will be extended to his relatively unknown successors. Berkshire's $380 billion portfolio makes it one of the world's largest active equity asset managers. Expecting a two-person team to replace Buffett and Munger, given the size, expectations, and accountability, is unrealistic.

Additionally, Berkshire should no longer be relied upon as the steadfast provider of liquidity it once was during times of crisis. In 2008, Warren Buffett sold significant portions of holdings in Johnson & Johnson, Procter & Gamble, and ConocoPhillips to buy billions in fixed-income securities with equity potential issued by Wrigley, Goldman Sachs, and General Electric. In addition, he wrote $40 billion worth of puts and credit default swaps. Buffett’s two-man successor team should never have the expectation of engaging in this level of tactical positioning.

Prescription

The prudent course of action is for Berkshire to sell down its concentrated positions, diversify, pay the capital gains tax owed, and return a large portion of the proceeds to shareholders. This would result in a smaller and more diversified portfolio thus greatly reducing significant portfolio risk and decision-making uncertainty by Buffett’s two-man succession team. We think Berkshire should go even further and strive to continue to diversify its holdings and even consider direct indexing strategies.

In a way, this shift has already taken place operationally. The investment portfolio once held a more prominent position within Berkshire's asset base. However, a pivotal turning point occurred after Berkshire acquired BNSF in 2009, which marked the onset of Berkshire's transformation from its core identity as an investment manager propelled by the large float from its insurance subsidiaries into a fully-fledged conglomerate. Since that milestone, Berkshire has consistently reinvested substantial resources into its diverse portfolio of subsidiaries, further emphasizing its conglomerate status.

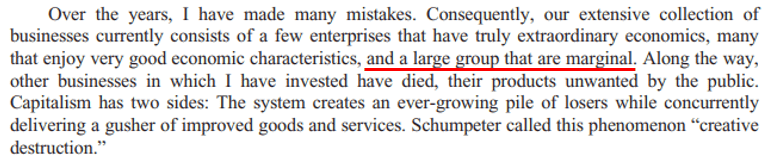

De-emphasizing the investment portfolio will also help Berkshire focus on what it needs to most: fixing, right sizing and enhancing its wholly owned subsidiaries. Below, Buffett alludes to some of the challenges faced with his subsidiaries. Note the change in wording from a "few that are marginal" to a "large group that are marginal."

Berkshire Hathaway 2021 10-k Annual Letter:

Berkshire Hathaway 2022 10-k Annual Letter:

Conclusion

We fully recognize the formidable challenge of de-emphasizing the investment portfolio, given its historical significance as Berkshire's secret sauce. Nevertheless, as Berkshire Hathaway transitions into its next phase, it becomes imperative to address the risks to its business model. The prospect of entrusting a $380 billion concentrated equity portfolio to a two-person team and hoping for a favorable outcome presents a significant and unaddressed risk. This need has become even more pressing since the passing of Warren Buffett's longtime partner, Charlie Munger. Today, it is crucial for Berkshire to take concrete and actionable steps to mitigate this risk and secure the company's sustained success.

INVESTMENT DISCLAIMERS & INVESTMENT RISKS

Past performance is not necessarily indicative of future results. All investments carry significant risk, and it’s important to note that we are not in the business of providing investment advice. All investment decisions of an individual remain the specific responsibility of that individual. There is no guarantee that our research, analysis, and forward-looking price targets will result in profits or that they will not result in a full loss or losses. All investors are advised to fully understand all risks associated with any kind of investing they choose to do.